The Standard Group Plc is a

multi-media organization with investments in media platforms spanning newspaper

print operations, television, radio broadcasting, digital and online services. The

Standard Group is recognized as a leading multi-media house in Kenya with a key

influence in matters of national and international interest.

For the best experience, please enable JavaScript in your browser settings.

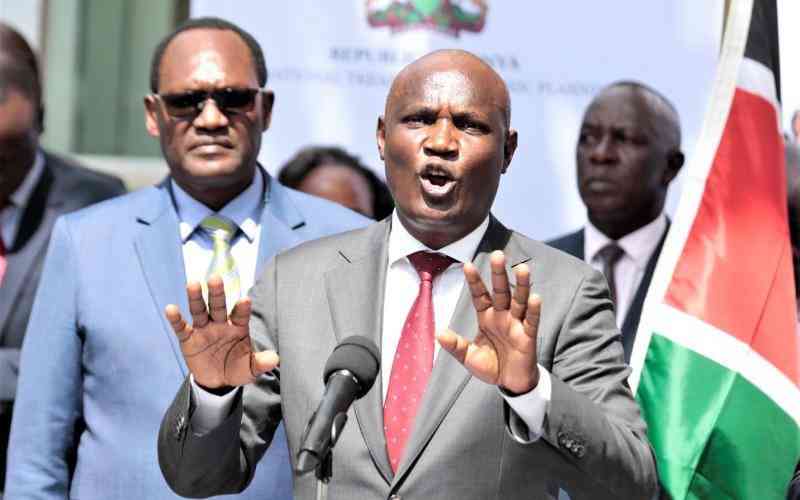

National Treasury CS John Mbadi(centre) accompanied by his PS Dr. Chris Kiptoo(left) with Economic Planning Principal Secretary, James Muhati(right) addressing the media outside Treasury Building in Nairobi on February 13, 2025, where they outline the progress made by the government in boosting momentum towards putting money in people's pockets. [Boniface Okendo, Standard]

On the day the government announced that it had issued another Eurobond, the National Treasury Cabinet Secretary John Mbadi painted a worrying picture of the country's debt situation.

Mbadi had particularly pointed out the impact the several Eurobonds, mostly taken by the Jubilee administration but also the Kenya Kwanza government, are having on the country’s fiscal space. The government onThursdaysaid it had issued yet another Eurobond and raised $1.5billion (Sh194 billion).

The CS termed Kenya’s as a “terrible situation”, noting that this was being seen not just in the size of the Eurobonds that are now starting to mature, one after the other but also the high interest rates that they attract.

These are concerns that have been raised by not just Mbadi but also other institutions including the Auditor General, civil society organisations and economists.

Despite the reservations, Mbadi had gone on to sign off on the new $1.5 billion Eurobond. It was also against earlier assertions by senior government officials, including President William Ruto, that the government would keep off costly loans from commercial lenders and instead focus on concessional multilateral and bilateral loans that offer low interest rates and longer repayment periods.

“When it comes to the repayment of Eurobonds, we are in a terrible situation. There is a Eurobond maturing in 2027 of $900 million (Sh117 billion). It is supposed to be repaid in three tranches of $300 million (Sh39 billion) each in 2025, 2026 and 2027,” he said.

The fresh Eurobond issued last week is expected to pay off the $900 million Eurobond taken in 2017. The new Eurobond however commits Kenya for another decade as it will be repaid in three tranches in 2034, 2035 and 2036.

“Then in February 2028, we are supposed to repay $1 billion (Sh129 billion) and then in 2031, we have $1.5 billion (Sh194 billion) and then in 2032, we have $1.2 billion (Sh155 billion) and in 2034, we have $1 billion (Sh129 billion) to pay.”

Other than Eurobonds, the other cadre of expensive loans that are starting to fall due are syndicated loans, which are loans from commercial banks with equally high interest rates.

“This year alone, we are supposed to repay syndicated loans of close to $1 billion (Sh129 billion) by October. In September, we are supposed to pay $200 million (Sh25.8 billion) to the Trade and Development Bank (TDB). We are also supposed to pay another €75 million (Sh10 billion) and in October $646 million (Sh83.33 billion). This goes on to 2030,” he said, adding that the worst is between now and 2034 when pressure on debt repayments should ease.

During the interview with Spice FM, however, Mbadi said the government had acquired a new debt that would further commit Kenya to 2036. Treasury would issue a statement later on Thursday informing the public it had taken the loans.

Mbadi blamed the Jubilee administration for the predicament that the country finds itself in. “We put ourselves in a situation where we took too many expensive loans over a period of time. This is especially between 2014/15, 2015/16 and got worse in 2016/17,” he said.

The Eurobond issued last week is perhaps the single largest loan and the most expensive that the government has taken since Mbadi took over as Treasury CS.

Despite this, he believes he is acting in the best interests of the country and that his successor will not have to confront the challenges and frustrations he is facing today on account of what his predecessors did.

Stay informed. Subscribe to our newsletter

“I want to try my best and leave this office better so that whoever comes in does not go through some of the stresses that I am going through,” he said.

“We need to get our systems right. One of the most critical steps is to have a system of managing our procurement because that is where we lose a lot of resources.”

Kenya issued the first $2 billion (Sh258 billion at the current exchange rate) Eurobond in 2014, which was at an interest rate of 6.875 per cent.

The second one of $900 million (Sh116.1 billion) was issued in 2017 with a coupon rate of seven per cent and matures in 2027 while a third in 2018, raised $2 billion (Sh258 billion) with an interest rate of 8.5 per cent.

The government in February last year issued another $1.5 billion (Sh194 billion) Eurobond with a coupon rate of 10.375 per cent and a maturity date of 2031. The latter was used to partly repay the $2 billion Eurobond taken in 2014.

The Public Debt Management Office said in a recent Debt Sustainability Analysis that “Kenya’s public debt is sustainable but with a high risk of debt distress”.

“The present value (PV) of public debt was 63 per cent of GDP against the benchmark debt threshold of 55 per cent of debt to GDP. The National Treasury has untilNovember 1, 2029, to bring the present value of public debt within the threshold to comply with the law.”

Kenya’s public debt stood at Sh10.79 trillion as of September 2024, according to Central Bank of Kenya data. It has grown by Sh2 trillion from Sh8.7 trillion in September 2022.

The debt to GDP ratio stands at 67 per cent over the current financial year against the legal requirement of 55 per cent. The Auditor General in a report in February last year noted that all indicators are that Kenya’s debt is getting to unsustainable levels, adding that the country’s appetite for eurobonds is a slippery slope.

“The office (of the Auditor General) has continually raised concerns over the growing level of public debt in Kenya,” said the Auditor General in the report.

The office further took issue with borrowing through Eurobonds that she noted are costly not just because of the higher interest rates but also due to other costs of issuing these bonds including commissions paid to companies that arrange them.

“The government of Kenya has now issued four Eurobonds each with a higher coupon rate reflecting the likely unsustainability of the current debt portfolio,” said the Auditor General when Kenya issued the $1.5 billion in February last year.

“The cost of these Eurobonds goes behind the interest rates. Issuing and servicing these debts involves additional fees and commissions. Additionally, fluctuations in foreign exchange rates impact the cost of repayment.”

“Kenya’s reliance on Eurobonds has raised concerns about debt sustainability,” said the Auditor General, adding about the vulnerabilities occasioned by maturing Eurobonds.

“While Eurobonds offer access to funds for development projects, managing repayment obligations remains a crucial challenge especially because of the shorter maturity periods and increasing coupon rates.

When the Treasury borrowed $1.5 billion last year in February through the issuance of a Eurobond, the Okoa Uchumi coalition noted that the debt acquisition trend had put Kenya on a dangerous path to destruction.

This, the coalition explained, was especially due to the continued disregard for the need for debt to have intergenerational equity as per the constitution of Kenya.

Okoa Uchumi noted that in taking new loans, the Public Finance Act requires that the government gets the lowest possible cost in the market. It noted that the interest rates for recent debt, especially Eurobonds, offered a huge return to private investors rather than looking at the bigger picture of the overall debt burden that is compounded by the pricing of the new Eurobond.

“Most importantly, we wonder when the Public Finance Act Section 15 (2) b on fiscal responsibilities that requires that in the medium term, all borrowing by the government be only for development initiatives and not recurrent is applicable,” said Okia Uchumi at the time.

“We also wonder when the law changed to allow for significant medium-term borrowing for debt servicing. The continued acquisition of debt on political and economic whims instead of legal and constitutional foundation is very concerning for a sovereign state.”

“The OKOA Uchumi Coalition calls on the Kenya government to look for the best financing strategies that will not result in increased debt distress because of short-term means of financing its development goals.”

Borrowing through Eurobonds has always been problematic since Kenya took the first such loan in 2014. Other than high interest rates, the government has in the recent past been borrowing to repay loans that are falling due.

The first Eurobond was subject to controversy, with a report by the Auditor General saying that its receipt and spending could not be ascertained.

In the April 2019 report following a special audit on the Eurobond taken in 2014, the Auditor General noted that the “utilisation of the proceeds of the Eurobond could not be traced to specific development projects. The National Treasury explained that these finds were fungible. Furthermore… some of the funds were expended outside of the government's Integrated Financial Management Information System (Ifmis).”

The Auditor General recommended that “subsequent issuance of international sovereign bonds should be earmarked and be identifiable to specific development projects”.

The Standard Group Plc is a

multi-media organization with investments in media platforms spanning newspaper

print operations, television, radio broadcasting, digital and online services. The

Standard Group is recognized as a leading multi-media house in Kenya with a key

influence in matters of national and international interest.

The Standard Group Plc is a

multi-media organization with investments in media platforms spanning newspaper

print operations, television, radio broadcasting, digital and online services. The

Standard Group is recognized as a leading multi-media house in Kenya with a key

influence in matters of national and international interest.