The Standard Group Plc is a

multi-media organization with investments in media platforms spanning newspaper

print operations, television, radio broadcasting, digital and online services. The

Standard Group is recognized as a leading multi-media house in Kenya with a key

influence in matters of national and international interest.

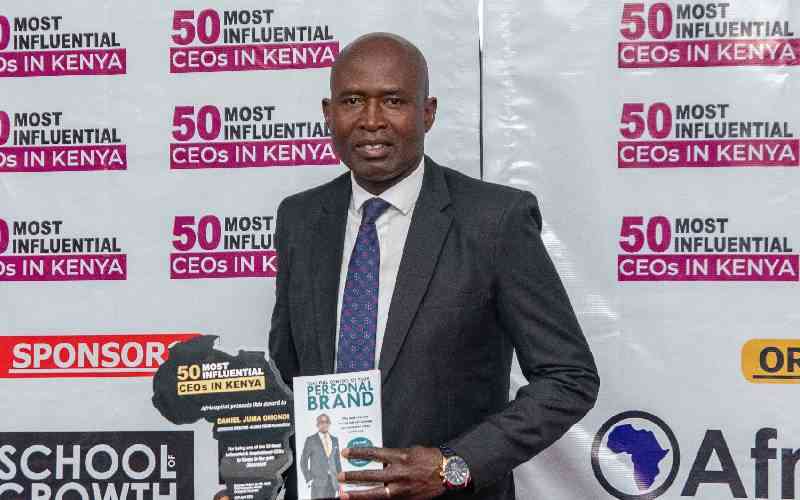

Kenya Re Managing Director Dr Hillary Wachinga. [Jonah Onyango, Standard]

Regional disparity in insurance sector standards forces Kenyan firms to incur extra costs to train staff in new markets where they set up subsidiaries.

These differences in the sector may be contributing to the slow pace of Kenyan insurance firms expanding to the rest of the region compared to banks.

Additionally, it explains why insurance penetration in Kenya, while low, is still above the rest of the markets whose numbers show they are below 1.0 per cent.

Kenya Reinsurance Corporation (Kenya Re) Group Managing Director Dr Hillary Wachinga says the firm has incurred extra costs to upskill its staff in new regional markets.

Dr Wachinga, while speaking on the sidelines of the CEOs Summit, which brought together chief executives of insurance businesses and regulators in Nairobi last week, said the region has a lot of disparities in standards.

This is even as he pointed out that Kenya is ahead of its peers when it comes to regulations in the sector.

“When you look at [the sector] cross-border, you find that you don’t have homogeneity in regulations,” he said.

“As reinsurers, we do technical seminars to upskill and upscale our counterparts in other countries. We are using our resources to develop other markets.”

He said this is to ensure the market is at par with Kenya. This challenge, he noted, does affect their operations in those new markets as clients sometimes do not understand why their practices are different.

Dr Wachinga gave an example of risk-based supervision (RBS), a framework in which he said while Kenya, particularly banks, adopted it way earlier, it has taken time for the insurance sectors in the region to do the same.

“Kenya adopted this quite a while back from the insurance industry’s perspective, but banks had already done it earlier under the sovereign requirement. If you look at other jurisdictions, they are still struggling,” he said.

He added: “At times because of this lack of uniformity, you may find our clients may not understand why we are doing what we are doing. We make them understand that we are not at par, and bringing them up to speed is quite important.”

The Kenya Re MD emphasised the need to harmonise regulations and even adopt the global best practices in the way these rules are implemented.

The lack of uniformity in regulations was one of the issues discussed at the summit, which attracted over 300 industry leaders across 83 countries.

Kenya Re boasts subsidiaries in Uganda, Ivory Coast, and Zambia. Apollo Group, easily identified as APA, and Jubilee Insurance also have businesses in Uganda and Tanzania.

Stay informed. Subscribe to our newsletter

Harmonisation of regulations in the financial services sector is one of the priorities of the East Africa Community (EAC).

Commissioner of Insurance and Chief Executive Insurance Regulatory Authority (IRA) Godfrey Kiptum said the region needs a robust and proactive regulatory framework, citing the challenges facing the sector.

These include climate change, technological advancements, and changing consumer needs.

Mr Kiptum said the global risks the industry faces demand for collaborative efforts of regulatory bodies at the international level.

“Forums such as the International Association of Insurance Supervisors and Financial Stability Board and other associations of regional regulators must share best practices, harmonise standards and develop early warning mechanisms to address systemic risks,” he said.

Insurance Regulatory Authority (Uganda) Alhaj Lubega said the market should evolve to accept policies across borders.

“Somebody in Uganda has medical insurance and is going to the Democratic Republic of Congo (DRC), Kenya, or Tanzania, but you will tell them that their policy only ends at the Ugandan border?” he posed.

National Treasury and Economic Planning Cabinet Secretary John Mbadi, who was the chief guest at the summit, said the government is dedicated to providing a conducive environment to ensure investment and growth in the insurance sector.

“Already, we have established a licensing regime to build and maintain confidence and make it easy for those interested in entering the market,” he said.

“The existing Insurance Act was also amended to improve regulatory oversight and enhance consumer protection.”

Director General Budget, Fiscal and Economic Affairs at the National Treasury Albert Mwenda said looking at how Kenyan banks have expanded to other markets, for their businesses to thrive, they need complementary services of the insurance sector.

“Some products will become more attractive if they are supplemented with the insurance industry,” he said.

According to the East Africa Insurance Outlook Report 2023 published by Deloitte, a financial consulting and advisory firm, total insurance penetration is at 1.2 per cent across the region, with insurance penetration in 2021 standing at 2.2 per cent in Kenya, 0.6 per cent in Tanzania, and 0.8 per cent in Uganda.

“The increasing demand for insurance products has seen improved regulation within the market to ensure consumer protections. One of the main drivers being capital and reserve requirements,” reads the report in part.

The Standard Group Plc is a

multi-media organization with investments in media platforms spanning newspaper

print operations, television, radio broadcasting, digital and online services. The

Standard Group is recognized as a leading multi-media house in Kenya with a key

influence in matters of national and international interest.

The Standard Group Plc is a

multi-media organization with investments in media platforms spanning newspaper

print operations, television, radio broadcasting, digital and online services. The

Standard Group is recognized as a leading multi-media house in Kenya with a key

influence in matters of national and international interest.