The Standard Group Plc is a

multi-media organization with investments in media platforms spanning newspaper

print operations, television, radio broadcasting, digital and online services. The

Standard Group is recognized as a leading multi-media house in Kenya with a key

influence in matters of national and international interest.

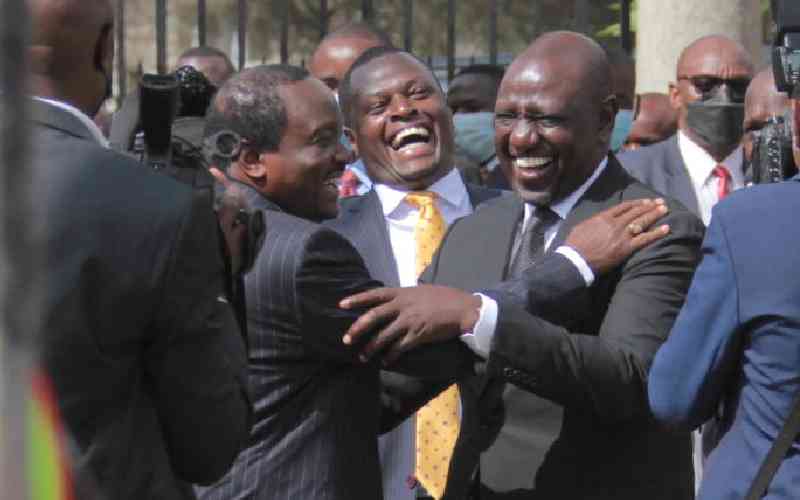

Samburu governor Lati Lelelit (second right) receiving a dummy cheque of Sh 10 million from officials of the Northern Rangelands Trust led by carbon credit project director Dr Mohammed Shibia (center) on February 28, 2024 in Maralal town. The money is proceeds from the large-scale grasslands soil carbon removal project in five community conservancies in the county. [Michael Saitoti, Standard]

More than a century after the scramble for Africa, a fresh dissection of the continent has emerged --this time as a result of climate change.

Reputable firms from wealthy nations in the East and West are signing long-term deals with African governments. Kenya has not been left behind in inking such agreements.

The emerging phenomenon has been triggered by global agreements on carbon credits to reduce greenhouse gas emissions. That was settled through the United Nations’ Intergovernmental Panel on Climate Change (IPCC) breakthrough at the 1997 agreement known as the Kyoto Protocol.

The carbon credit mechanism was strengthened through adoption by negotiators at the Glasgow COP26 climate change summit in November 2021 to create a global carbon credit off-set trading market.

The creation of the credit offset trading market has seen an increased interest in the purchase of carbon credits from Africa, given that the continent still falls under the least emitters of greenhouse gases.

Unlike the 19th-century scramble that originated from the West, firms from the Middle East and Asia are leading in the carbon trading.

One firm, Blue Carbon, under Sheikh Ahmed Dalmook Al Maktoum, an Emirate royal and Second Deputy Ruler of Dubai, has dominated the field.

Blue Carbon has signed deals with seven African countries and also acquired thousands of hectares of land in the continent.

Blue Carbon says, on its website, that it seeks to accelerate the global transition to a de-carbonised economy using bilateral agreements to help governments and its clients design and implement carbon abatement strategies in compliance with the Paris Agreement.

It notes that Blue Carbon was formed to create environmental assets, and nature-based solutions and register carbon removal projects using modern methodologies.

From Kenya to Tanzania, Liberia, Comoros, Zimbabwe, Zambia and Niger, Blue Carbonhas entered into Memoranda of Understanding (MOUs) that could last several years.

In September last year, Kenya, joined a growing list of African countries embracing carbon trading rules to govern domestic trade in carbon and tap into a $2 billion market after President William Ruto signed into law the Climate Change (Amendment) Bill 2023. This allowed the country to set up a national carbon registry and appoint an authority to run it.

During the opening of the inaugural Africa Climate Summit in Nairobi, Ruto said the time was ripe for Kenya and Africa to start monetizing its massive carbon sinks.

“We have the carbon sink that serves the world, cleans our environment, acts as sequestration of carbon that is produced by others but we get nothing for it. It’s not anywhere in our balance sheet. The day we put our whole assets in our balance sheet, you will know we are a very wealthy continent,” Ruto said.

Stay informed. Subscribe to our newsletter

In November last year, The Standard established that Kenya signed an MoU with Blue Carbon under the Framework of Collaboration (FOC) for the development of Reducing Emissions from Deforestation and Forest Degradation (REDD+) projects and carbon credit.

Interestingly, the government has not sought parliamentary approval on the MoU between Kenya’s State Department of Environment and Climate Change and the Dubai-based firm that the country would concede “millions of hectares” for production of carbon credit.

Through the REDD+ deal between the Dubai firm and Kenya, the credits would be generated supposedly from restoring and protecting the land, and the company would then sell these on to major polluters to offset their emissions.Kenya is not alone, such contracts between Blue Carbon and other African countries including Liberia, Tanzania, Zambia, and Zimbabwe abound, with the glaring one where Zimbabwe ceded 7.5 million hectares, a fifth of its landmass, to the UAE royal company.

Investigations indicate that Blue Carbon alone has control of over 24.5 million hectares in Africa, which includes land used by local communities. On their website, the Dubai based firm offers little information on the nature and terms of the deal, only noting that the contracts are meant to curb emissions.

What raises eyebrows is that Blue Carbon was registered in November 2022, according to details on its website, and entered into multi-trillion-dollar contracts with the African countries barely a year into its existence.

Not knowing the worth

As happened during the partition and scramble for Africa beginning in 1884 where African countries did not know their potential and natural wealth, most African countries have not measured their carbon credits and are selling a commodity they do not know its quantity.

According to Kenya Institute for Public Policy Research and Analysis, the major obstacle facing carbon markets in Africa is the scarcity of climate data and analytical capabilities across the continent.

For example, lack of accurate information on critical factors such as deforestation rates, renewable energy potential, and greenhouse gas emissions impedes the identification of viable carbon offset projects.

Additionally, data scarcity obstructs project feasibility assessments, effective intervention design, and the quantification of potential carbon reductions.

Further, the limited availability of data complicates the verification of actual carbon credits generated by projects, making it difficult to rigorously monitor progress. Consequently, this raises concern about project effectiveness and transparency, making it difficult for carbon buyers to assess the credibility and impact of offset projects and justify investor support in the region.

Noting the challenge, the Ugandan government in February signed a deal with Luokong Technologies with undertakings in Africa represented by Shiftings Ltd owned by Cyrus Jirongo for the deployment of a cutting-edge Digital Measuring, Reporting, and Verification (DMRV) platform.

Through the use of remote sensing technology, the platform, will measure Uganda’s carbon footprint, to allow the Ugandan government to drive for enhanced efficiency, transparency, and integrity in carbon-related initiatives.

President Yoweri Museveni presided over the signing of the deal between Uganda and Luokong Technology Corporation on February 3, 2024 at State Lodge Nakasero.

Luokong Technology Corporation is represented in Africa by Nairobi-based Shiftings Limited, owned by Cyrus Jirongo.

“We’re thrilled to introduce advanced tools to Africa’s carbon market, ensuring standardised, digitally-driven carbon accounting for nature-based projects at a fraction of traditional costs and time,” Jirongo told The Standard in an interview.

Jirongo said the problem with most of the African countries was them getting into carbon trading without knowing their worth thus getting prone to poor negotiations.

“In Uganda, the Democratic Republic of Congo, and a number of the countries we are in talks with, we want to help them know their potential so that they can trade from a point of knowledge,” said Jirongo.

Jirongo said that through the use of state-of-the-art satellite imagery, remote sensing, and machine learning technologies, their firms will provide Carbon Neutrality Data Services and Natural Resources Asset Management to assess and monitor Uganda’s carbon reserves.

“Our MoU focused on three key objectives including quantifying Uganda’s total carbon assets, establishing African standards for carbon quantification and accounting, and launching a carbon asset exchange - a trading platform in Kampala - to facilitate carbon asset trading among African nations and asset owners,” said Jirongo.

Jirongo said that despite recent technological strides, most African countries were still using conventional tools such as PDF files, spreadsheets, and manual measurements in forest carbon credit measurement and verification.

“The digital platforms we will use will automate and standardise data collection, analysis, and validation, ensuring objectivity, transparency, and significant reductions in time and costs associated with issuing new carbon credits—a pressing challenge in today’s carbon market landscape,” said Jirongo.

Late last year, concerned about the infiltration of foreign firms into the carbon trading business, Tanzania’s President Samia Suluhu asked her East African Community (EAC) counterparts to take a common stance in opposing the dominance of foreign companies in the region’s carbon trading.

Suluhu spoke at the EAC climate change and food security forum at Arusha and noted that the region needed to be wary reap-offs from carbon trading, by foreign firms.

“We need to be careful with some conditions from the Western world who want to use our environment for their benefit and not ours, especially through carbon trading programmes. Let’s have one position so that we find a way to conserve our environment. Not that we’re conserving, then foreign companies come to reap more than we’re reaping ourselves. No.” Suluhu told the EAC heads of State and governments.

The Standard Group Plc is a

multi-media organization with investments in media platforms spanning newspaper

print operations, television, radio broadcasting, digital and online services. The

Standard Group is recognized as a leading multi-media house in Kenya with a key

influence in matters of national and international interest.

The Standard Group Plc is a

multi-media organization with investments in media platforms spanning newspaper

print operations, television, radio broadcasting, digital and online services. The

Standard Group is recognized as a leading multi-media house in Kenya with a key

influence in matters of national and international interest.